Loan Denied? It's Not You, It's Your Messy Books (And We Can Fix It!)

The Real Reason Your Business Loan Was Denied

If you're a business owner, you know the feeling. You worked hard to create a business plan, you filled out all the forms, and you waited. Then, you got the letter: "Your loan application has been denied."

This can feel like a punch in the gut. It makes you ask, "Why not me? Is my business not good enough?"

The truth is, it's probably not you. It's not your business idea. It's not your hard work. It's something much simpler: your bookkeeping.

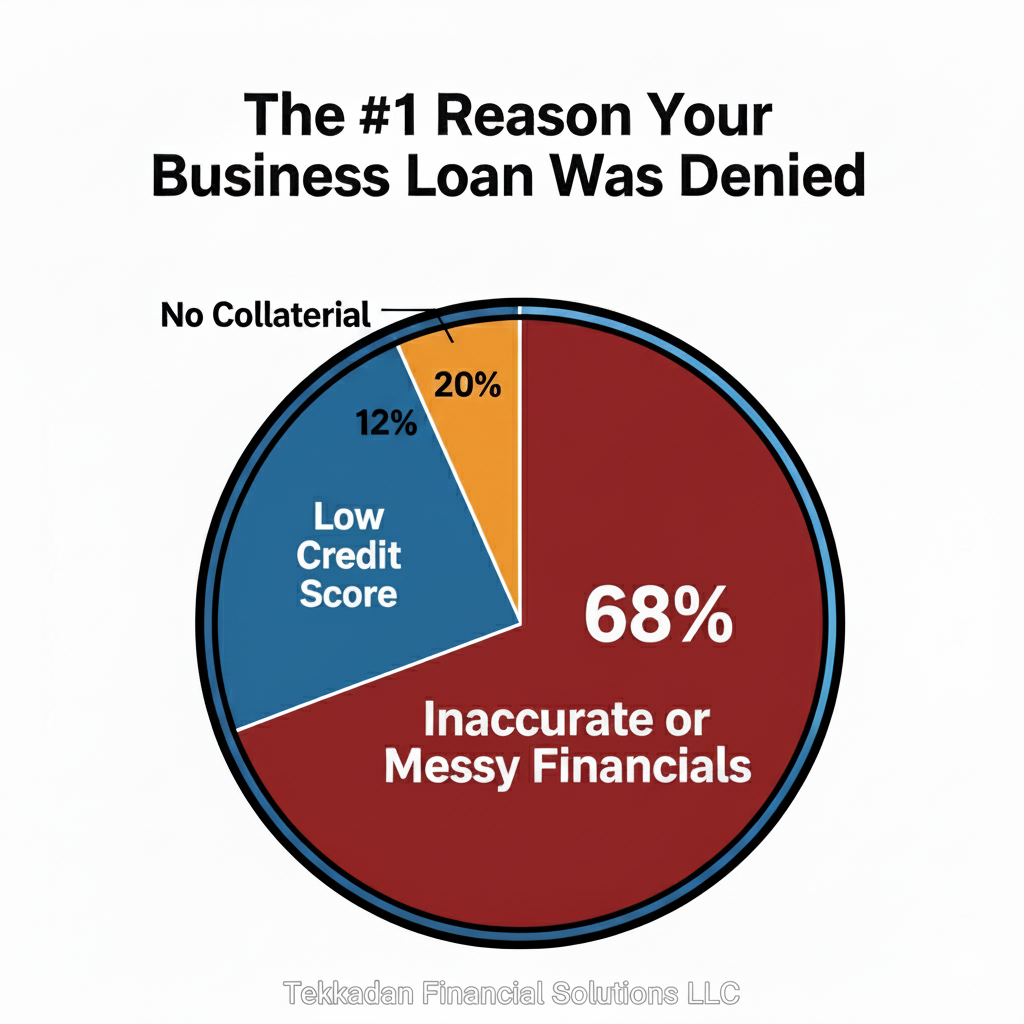

A study by the Federal Reserve Bank of New York found that 68% of small business loan applications are rejected because of problems with the borrower's financials [1]. The bank doesn't want to say your books are a mess. They just say, "You didn't meet our requirements."

But what does that mean? It means the bank couldn't trust your numbers. It means your messy books were the real reason your loan was denied.

The 5 Ws of Messy Books

To get a loan, you must show the bank that your business is safe to invest in. They do this by looking at your numbers. They want to know:

- How much money you have.

- How much money you owe.

- How much money you are making.

Messy books make it impossible for them to know these things for sure. Let's break down the problem with the 5 Ws.

- What are messy books? They are financial records that are not clean or correct. This includes numbers that don't match, missing receipts, and mixing business and personal money.

- Why are messy books a problem? They make your business look risky. A bank can't trust numbers that don't make sense, and they will think, "If the business owner can't keep their books straight, how can they manage a loan?"

- Who does this affect? It affects small business owners who are great at their job but are held back by financial chaos.

- Where does this problem start? The problem often starts in accounting software like QuickBooks. Without a good setup, it is easy to make small mistakes that grow into big problems. A study by LLC Buddy found that 44% of small businesses have cash flow problems because of messy books [2].

- When do you need to fix this? The answer is right now. Don't wait until you need a loan. By the time you need to apply, it may be too late. The time to get your books in order is before a bank or investor asks for them.

How to Fix Your Books (And Get Ready for Your Loan)

Now that you know the problem, here is a clear plan to fix it. This is your path to getting the money you need to grow.

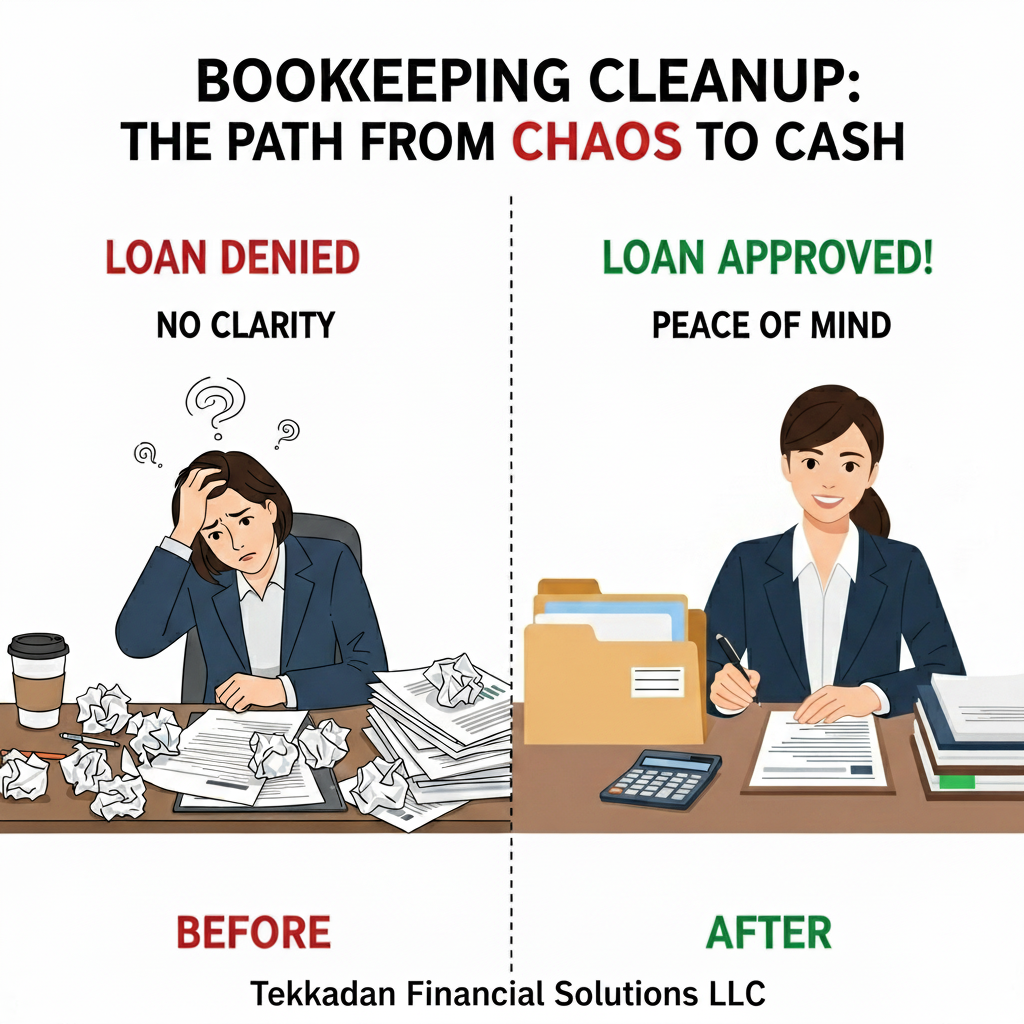

Step 1: The Bookkeeping Cleanup

Your first step is to fix your old financial records. This is like doing a deep clean on your business's books.

- What it is: A professional goes through months or even years of messy records. They find mistakes, match up your bank statements, and make sure every number is in the right place.

- Why it's important: It gives you a true picture of your business's past. When your books are clean, you can finally see how much money you have been making and where your money has gone.

You can't get a loan with messy books. It's like trying to build a house on a shaky foundation. A bookkeeping cleanup gives you a strong foundation to build on.

Step 2: Get Your Books Loan-Ready

Once your books are clean, you need to keep them that way. This is where you move from fixing the past to building a better future.

- What it is: This is a process of getting your books to a high level of accuracy. This includes things like financial reporting and analysis. You get reports that tell you how your business is doing in a clear way.

- Why it's important: It gives you a clear and honest picture of your business's health. Lenders and investors need to see a clean balance sheet, income statement, and cash flow statement. 27% of micro-business loan applications are rejected because lenders can't confirm their financial data [3]. This step makes your numbers clear and trustworthy.

Step 3: Get an Expert to Guide You

You are an expert at your business. Let a financial expert be an expert in your business's money.

- What it is: A financial expert can work with you to plan your funding journey. They can help you prepare your loan application and connect you with the right people. This is a part of our business funding advisory service.

- Why it's important: With an expert, your loan application won't be a guess. It will be a professional presentation of your business's health, giving you the best chance of getting approved.

Frequently Asked Questions (FAQ)

Q: What do banks look at in my financials?

A: Banks look at a few main things. They want to see your Income Statement to know if your business is making money, your Cash Flow Statement to make sure you have enough cash to pay them back, and your Balance Sheet to see what you own and what you owe. Having clean, clear financial reports is a must.

What does it mean to be "loan-ready"?

Being loan-ready means your business has a clean and clear financial story. It means your records are organized, your numbers are correct, and you have all the reports a bank will ask for. This is a big step toward getting approved.

How can bookkeeping cleanup help me get funding?

A cleanup gives you accurate reports. These are the same reports that a bank uses to decide if you are a good person to lend money to. With a cleanup, your numbers will be clean and trustworthy.

How can I keep my books clean every month?

The best way is to have a system. You can use software like QuickBooks, but it is best to have a professional do a monthly check-in to make sure everything is perfect.

What if I've been doing my own books for years?

That's okay. Many business owners try to do their own books. The most important thing is to get them in great shape now so you can stop worrying about them.

My credit score is bad. Can I still get a loan?

Yes. Many small business loans look more at your company's books and its cash flow than just your personal credit score. Getting your business's financials in order is a great first step.

What is a business funding advisory service?

This is a service that helps you get ready for funding. It includes making sure your financials are perfect, helping you understand your options, and even connecting you with lenders. It's a key part of your funding journey.

What if my business has no credit history yet?

That's okay. Many small businesses do not have a credit history. In this case, a lender will look even more closely at your company's financial reports to decide if you are a good risk. Having clean books is the most important thing you can do.

What is the most common mistake in a loan application?

The most common mistake is a messy or incomplete financial statement. It is a very easy way to get a loan denied, and it is a problem that can be fixed. In fact, 68% of small business loans are rejected because of issues with the borrower's financials [1].

What is a balance sheet, and why do banks care about it?

A balance sheet is a report that shows everything your business owns and everything it owes. Banks look at it to see how strong your business is. It helps them decide if your business is financially healthy enough to get a loan.

Ready to Transform Your Business Finances?

Don't let financial management hold your business back another day. Whether you need help with bookkeeping cleanup from experienced professionals, or you want to work with a trusted advisor that local business owners recommend, Tekkadan Financial Solutions LLC is here to help.

Call us now to schedule your free quote. Your business deserves professional financial management – let's make it happen together.

Visit our homepage for more information on how we can be your financial partner: Tekkadan Financial Solutions LLC

Disclaimer: This article is for general information only and does not constitute professional accounting or legal advice. You should always consult with a qualified professional to discuss your unique situation.

Sources

[1] Federal Reserve Bank of New York. "Small Business Credit Survey: 2024 Report on Employer Firms." Research found that issues with a firm's credit score and poor financials are the leading cause of loan rejections. [2] LLC Buddy. Data on challenges faced by small and medium-sized businesses. [3] Small Business Administration (SBA). Research on factors for small business loan approval. [4] Forbes Advisor. "Why a Small Business Loan Might Be Denied." Article highlights common reasons for loan denial, including incomplete or inaccurate financial statements. [5] Inc. Magazine. "What Lenders Look for in Financial Statements." Article provides a breakdown of how lenders assess a company's financial health based on their books. [6] Business Dasher. Statistics on QuickBooks usage and small business accounting. [7] Clutch.co. Research on why small businesses lack accounting resources.